Since the end of June, SHFE tin prices have fluctuated between 260,000 yuan/mt and 270,000 yuan/mt, with a very stagnant trend. Trading volume has also continued to contract, and market attention has decreased. The volatility index for SHFE tin options, VIX, has dropped to its lowest level in nearly a year. So, what factors have led to the significant narrowing of SHFE tin's trading range? What are the key points to watch in the future?

Data source: Webstock Inc.

Slow Resumption of Tin Ore Production in Myanmar Hinders Supply Recovery

The resumption of tin ore production in Myanmar has been slow. On July 15, a public meeting was held in the Lower Burma region, where several companies' applications for mining licenses (valid for three years) were approved. It is understood that after completing the payment of management fees and clearing physical taxes, these companies will gradually resume normal mining operations, and the local mining production order is gradually being restored. Currently, there are signs of easing supply constraints for critical materials needed for mine resumption (such as mining equipment and explosives). However, due to the rainy season, earthquakes, and mine preparation, actual ore output is expected to be delayed until Q4.

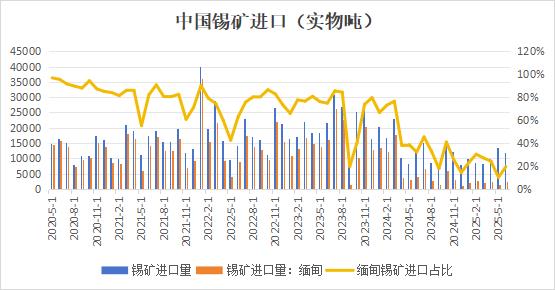

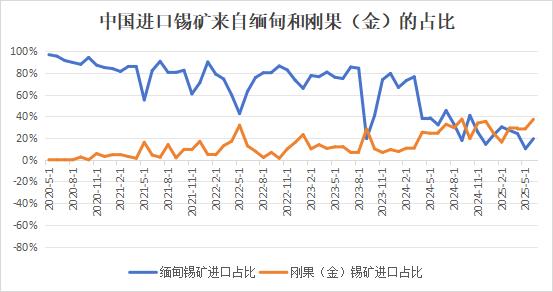

China's tin ore imports remain low. According to data from the General Administration of Customs, cumulative tin ore imports in H1 2025 were approximately 62,100 mt in physical content, up 3.04% YoY. In June, tin ore and concentrate imports amounted to 11,911.43 mt in physical content (equivalent to 5,656.91 mt in metal content), up 20.87% YoY but down 16.28% MoM. Imports from Myanmar in June were 2,314 mt, accounting for 19%. Africa has become an important source of imports, with increased African tin ore imports partially offsetting the shortfall from Myanmar. Alphamin Resources, a major tin producer in DRC, experienced a short-term shutdown in late March due to geopolitical conflicts, leading to expectations of tighter domestic mine supplies and a noticeable decline in tin ore exports in March-April. However, after resuming production, there have been no obstacles, and over 80% of the output is shipped to Chinese ports. Tin ore imports from DRC to China significantly rebounded in May-June.

Data source: General Administration of Customs

Data source: General Administration of Customs

Due to tight raw material supplies, smelters' operating rates have remained at low levels. According to SMM's in-depth market survey and processing data, as of August 15, the combined operating rate of refined tin smelters in Yunnan and Jiangxi provinces rose to 59.23%, dropping back slightly MoM. This continues the trend of low operating rates seen since the beginning of the year. In Yunnan, the rigid constraint of raw material shortages has intensified, with tin ore inventories at smelters generally below 30 days. Intense competition for procurement has driven up processing costs for low-grade ores, coupled with rising power costs, leading to low production willingness. Some manufacturers have planned maintenance shutdowns to clear intermediate products and barely maintain limited output. Jiangxi region faces the dilemma of a broken scrap tin supply chain. The adjustment of glass production lines in 2024 led to a reduction in the clearance volume of tin scrap, while enterprises using tin scrap to produce crude tin expanded their scale, resulting in an undersupply of tin scrap. On the other hand, the US imposed additional tariffs on Chinese consumer electronics components, including key downstream products like tin solder, leading to a sharp decline in traditional solder export orders and a contraction in downstream enterprise production, causing a sudden drop in tin scrap generation. The circulation of secondary materials in the market decreased by more than 30% YoY, severely restricting the recovery of refining capacity due to a severe shortage of crude tin supply. Although some recycled tin enterprises attempted to gradually resume production after maintenance, the overall capacity increase was slow due to the obstruction of the scrap recycling system. In the short term, the slow resumption of mining operations in Myanmar's Wa State and the continued disruption of land transportation from Thailand limit import supplements, while the Jiangxi scrap recycling system remains unrepaired. Coupled with processing fees remaining at a historically low level of 11,000 yuan/mt, enterprises are forced to reduce their capacity utilization rate to 30-40%. If there is no substantial improvement in raw material supply, there is still a risk of further decline in operating rates.

Downstream demand in off-season, cautious market purchases

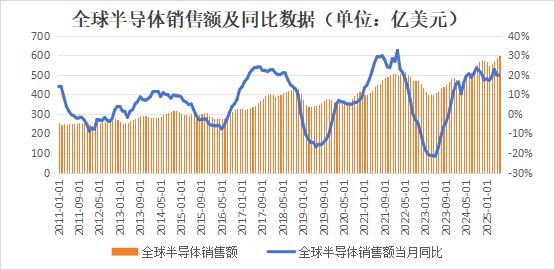

Tin downstream order levels continue to decline, and Q3 is the off-season for downstream consumption, with tin-related consumption lower than in previous years, and insufficient home appliance production schedules. The spot tin market maintains a weak supply and demand situation, with traders following the market, and brands with relatively small premiums selling better. Smelters mostly show reluctance to budge on prices, while downstream buyers enter the market to purchase at low points. In the semiconductor sector, according to data from the US Semiconductor Industry Association (SIA), global sales reached $59.9 billion in June 2025, up 19.6% YoY and 1.5% MoM. For the full year, the World Semiconductor Trade Statistics (WSTS) forecasts that the global semiconductor market size will reach $700.9 billion in 2025, up 11.2% YoY. WSTS believes that this year's growth in the semiconductor market size will be led by increases in logic and memory; both markets are driven by sustained demand in areas such as AI, cloud infrastructure, and advanced consumer electronics. WSTS also notes that although the overall market is expanding, it is expected that some product segments will continue to shrink. For example, discrete semiconductors, optoelectronic devices, and micro ICs are expected to see a low single-digit decline. These declines are mainly attributed to ongoing trade tensions and negative economic development trends, which have disrupted the supply chain and suppressed demand in specific application areas.

Data source: US Semiconductor Industry Association

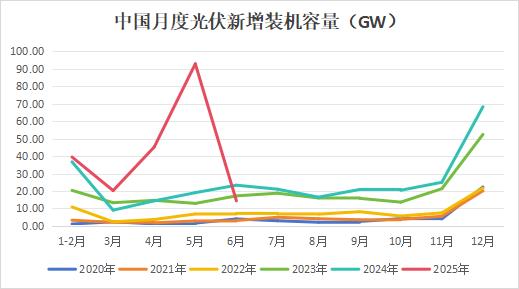

In the PV sector, after the mid-year installation rush, new PV installations in June declined. According to statistics released by the National Energy Administration, new PV installations in June 2025 were 14.36 GW, down 38% YoY. However, in H1 2025, China's new PV installations exceeded the 200GW mark, reaching 76.53% of last year's total. Due to a significant MoM decline in PV orders, overall demand for tin used in PV solder remained weak.

Data source: National Energy Administration

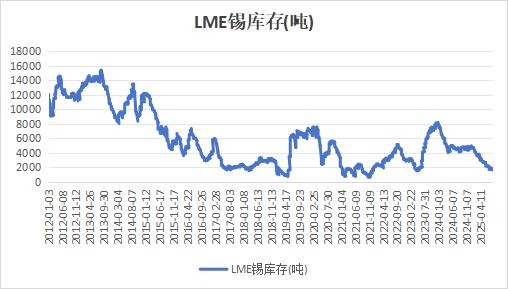

Overseas semiconductors are mainly focused on advanced processes, while China's semiconductor industry has a more complete mature process industry chain. In recent years, the vigorous development of the artificial intelligence industry has primarily driven a substantial increase in demand for advanced processes such as GPUs. Demand growth for consumer electronics and automotive electronics related to mature processes has been relatively stable. Strong overseas demand also led to continuous destocking of LME tin ingot inventory. As of August 15, LME tin inventory fell to 1,655 mt, down 3,145 mt from the beginning-of-year level of 4,800 mt, a decrease of 65%, reaching the lowest level since 2023. In contrast, domestic social inventory experienced a noticeable destocking in H2 last year but has started to build up again this year. As of August 15, China's social inventory of tin ingots was 10,392 mt, an increase of 56% from the beginning of the year. Low LME tin inventory, along with issues of concentrated open interest and changes in macro sentiment, can easily lead to increased price volatility in LME tin, thereby affecting SHFE tin prices. Caution is advised against the risks brought by low LME inventory.

Data source: London Metal Exchange

Looking ahead, short-term tin ore supply is unlikely to see a significant increase, and the issue of tight supply remains unresolved. Currently, it is the off-season for consumption, and overall demand is relatively weak, with both supply and demand being weak, leading to continued sideways movement in tin prices with limited upside and downside. However, the problem of low LME tin inventory cannot be ignored, and caution is advised against potential price fluctuations caused by speculative activities. In the medium and long-term, as the supply of tin ore from Myanmar gradually recovers, the tight supply and demand situation will ease, and the price center of SHFE tin may shift downward.

(Comprehensive by Wenhua)

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)